3 Affordable Pharma Stocks to Buy for Portfolio Gains

The pharmaceutical market is anticipated to grow substantially in the upcoming years, owing to technological innovation and rising demand for personalized medicines. To that end, affordable pharma stocks ACADIA Pharmaceuticals (ACAD), Astellas Pharma (ALPMY), and Spero Therapeutics (SPRO), trading under $20, could be solid buys now. Read on….

The pharmaceutical industry is undergoing a transformative boom, leveraging digital platforms, big data analytics, cloud computing, and AI to drive innovation. Moreover, the growing demand for personalized drugs and increased R&D activities should give an additional boost to the already burgeoning industry.

Therefore, fundamentally robust pharma stocks ACADIA Pharmaceuticals Inc. (ACAD), Astellas Pharma Inc. (ALPMY), and Spero Therapeutics, Inc. (SPRO), trading under $20, could be wise portfolio additions now.

The global use of medicines increased by 14% over the past five years, and a 12% rise is anticipated through 2028, bringing annual usage to 3.80 trillion defined daily doses. The growing prevalence of chronic diseases and rising demand for medical care amid the increasing aging population have contributed to the pharmaceutical market’s resilience in the future.

With the rise in demand for treating chronic diseases such as cancer, diabetes, and more, along with increased R&D activity for new drugs and treatments, the drug discovery informatics market is projected to reach $7.90 billion by 2032, growing at a 10.5% CAGR. These growing trends also include the growth and demand for personalized medicine, which has bolstered the pharma market.

As per the American Society of Health-System Pharmacists, the ongoing drug shortages in the U.S. have reached an all-time high since 2001, at 323 drugs at the end of the first quarter this year. With the growing demand for drugs, this shortage will potentially boost prices.

Moreover, pharmaceutical firms are adopting tech for personalized drug production, requiring adaptable facilities. In 2023, AI emerged as crucial in drug discovery, and it is expected to continue enhancing research efficiency in 2024.

Considering these conducive trends, let’s take a look at the fundamentals of the three Medical – Pharmaceuticals stocks, beginning with the third choice.

Stock #3: ACADIA Pharmaceuticals Inc. (ACAD)

ACAD develops and commercializes innovative medicines that address unmet medical needs in central nervous system (CNS) disorders and rare diseases in the U.S.

In terms of forward EV/Sales, ACAD is trading at 2.62x, 25.9% lower than the industry average of 3.54x. The stock’s forward Price/Sales multiple of 3.02 is 17.8% lower than the industry average of 3.67.

Over the past three and five years, its revenue grew at CAGRs of 18% and 26.6%, respectively, while its total assets grew at a 6.8% CAGR over the past five years.

For the fiscal fourth quarter that ended December 31, 2023, ACAD’s total revenues increased 69.3% year-over-year to $231.04 million. Moreover, its income from operations came to $34.94 million, compared to a loss from operations of $46.06 million in the prior-year quarter.

For the same quarter, its net income and earnings per share stood at $45.80 million and $0.28, compared to net loss and net loss per share of $41.73 million and $0.26, respectively.

Street expects ACAD’s revenue for the fiscal first quarter that ended March 2024 to increase 76.3% year-over-year to $208.82 million. Its EPS is expected to be $0.06 for the same quarter. The company surpassed consensus revenue estimates in three of the trailing four quarters, which is impressive.

The stock has declined 1.8% intraday to close the last trading session at $17.41.

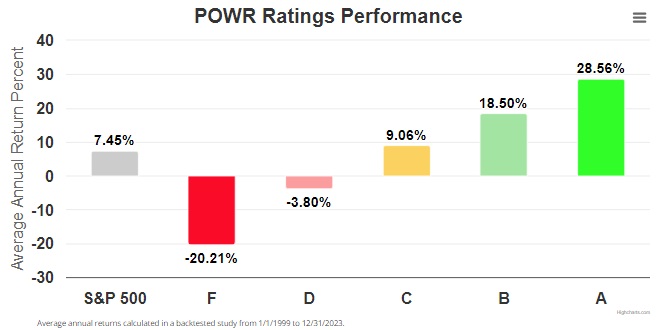

ACAD’s POWR Ratings reflect its positive prospects. The stock has an overall B rating, equating to Buy in our proprietary rating system. The POWR Ratings are calculated by considering 118 distinct factors, with each factor weighted to an optimal degree.

ACAD has an A grade for Growth and a B for Value and Quality. Within the Medical – Pharmaceuticals industry, it is ranked #28 out of 160 stocks.

To see additional POWR Ratings for Momentum, Stability, and Sentiment for ACAD, click here.

Stock #2: Astellas Pharma Inc. (ALPMY)

Headquartered in Tokyo, Japan, ALPMY manufactures, markets, and imports and exports pharmaceuticals in Japan and internationally. The company mainly operates Pharmaceutical Products business segment.

On March 28, ALPMY announced that the Center for Drug Evaluation (CDE) of the China National Medical Products Administration (NMPA) accepted the supplemental Biologics License Application (sBLA) for enfortumab vedotin with KEYTRUDA (pembrolizumab) as a combination therapy for the first-line treatment of adult patients with previously untreated locally advanced or metastatic urothelial cancer (la/mUC).

If approved, enfortumab vedotin with KEYTRUDA has the potential to change the treatment paradigm, becoming the first combination treatment to offer an alternative to platinum-containing chemotherapy, the current standard of care in first-line la/mUC.

On March 26, ALPMY announced that the U.S. Centers for Medicare and Medicaid Services assigned a unique, permanent Healthcare Common Procedure Coding System (HCPS) J-code for IZERVAY (avacincaptad pegol intravitreal solution) for the treatment of geographic atrophy secondary to age-related macular degeneration. The new J-code, J2782, is effective since April 1.

Its annualized dividend rate of $0.47 per share translates to a dividend yield of 4.62% on the current share price. Its four-year average yield is 2.76%.

In terms of forward EV/Sales, ALPMY is trading at 2.17x, 38.7% lower than the industry average of 3.54x. The stock’s forward Price/Sales multiple of 1.80 is 51.1% lower than the industry average of 3.67.

Over the past three and five years, its revenue grew at CAGRs of 7.2% and 3.4%, respectively, while its total assets grew at 13.6% and 11.8% CAGRs over the same periods.

For the nine months that ended December 31, 2023, ALPMY’s revenue and gross profit increased 2.1% and 3.4% year-over-year to ¥1.19 trillion ($7.77 billion) and ¥969.81 billion ($6.33 billion), respectively. Moreover, its core operating profit stood at ¥149.62 billion ($977.26 million).

For the same period, its core profit and basic core earnings per share stood at ¥120.51 billion ($787.09 million) and ¥67.20, respectively.

Street expects ALPMY’s revenue for the fiscal year that ended March 2024 to increase 124.2% year-over-year to $10.27 billion. Its EPS is expected to be $0.24 for the same period. The company surpassed consensus revenue estimates in three of the trailing four quarters.

The stock has gained marginally intraday to close the last trading session at $10.29.

ALPMY’s POWR Ratings reflect this promising outlook. It has an overall rating of B, which translates to a Buy in our proprietary rating system.

ALPMY has an A grade for Stability and a B for Value. Within the same industry, it is ranked #21.

For ALPMY’s other ratings (Growth, Momentum, Sentiment, and Quality), click here.

Stock #1: Spero Therapeutics, Inc. (SPRO)

SPRO identifies, develops, and commercializes novel treatments for multi-drug resistant (MDR) bacterial infections and rare diseases in the U.S.

On February 28, SPRO received clearance by the U.S. Food and Drug Administration (FDA) for its investigational new drug application, to evaluate SPR206 in a Phase 2 clinical study. SPR206 is a novel, intravenously (IV) administered next-generation polymyxin antibiotic for the treatment of hospital-acquired and ventilator-associated bacterial pneumonia caused by MDR Gram-negative bacterial infections.

On January 2, SPRO announced the first patient, first visit for PIVOT-PO, a global pivotal Phase 3 clinical trial of tebipenem HBr in patients with complicated urinary tract infections, including acute pyelonephritis.

In terms of forward EV/Sales, SPRO is trading at 0.43x, 87.8% lower than the industry average of 3.54x. The stock’s forward Price/Sales multiple of 1.90 is 48.3% lower than the industry average of 3.67.

Over the past three and five years, its revenue grew at CAGRs of 123.2% and 92.1%, respectively, while its total assets grew at 5.9% and 7.2% CAGRs over the same periods.

For the fiscal fourth quarter that ended December 31, 2023, SPRO’s total revenues and net income attributable to common shareholders of SPRO increased 55% and 91.2% year-over-year to $73.52 million and $51.19 million, respectively.

As of December 31, 2023, SPRO’s total current assets, and accrued expenses and other current liabilities amounted to $131.21 million and $6.56 million, compared to $113.57 million and $8.97 million as of December 31, 2022, respectively.

Street expects SPRO’s revenue for the fiscal first quarter that ended March 2024 to increase 940.8% year-over-year to $21.53 million. The company surpassed consensus revenue estimates in each of the trailing four quarters and consensus EPS estimates in three of the trailing four quarters.

The stock has gained 46.2% over the past six months to close the last trading session at $1.71. Over the past three months, it has gained 17.1%.

SPRO’s robust prospects are reflected in its POWR Ratings. The stock has an overall B rating, equating to Buy in our proprietary rating system.

SPRO has an A grade for Value and a B for Sentiment and Quality. It is ranked #18 within the same industry.

Click here for the additional POWR Ratings for SPRO (Growth, Momentum, and Stability).

What To Do Next?

43 year investment veteran, Steve Reitmeister, has just released his 2024 market outlook along with trading plan and top 11 picks for the year ahead.

ALPMY shares were unchanged in premarket trading Friday. Year-to-date, ALPMY has declined -13.53%, versus a 9.32% rise in the benchmark S&P 500 index during the same period.

About the Author: Neha Panjwani

From her school days, Neha harbored a profound fascination for finance, a passion that steered her toward a career as an investment analyst following the completion of her bachelor’s degree in commerce. Currently enrolled in the CFA program, Neha is dedicated to further enriching her comprehension of investment fundamentals. Neha’s primary objective is to aid retail investors in discerning optimal investment opportunities by diligently evaluating crucial aspects of financial instruments, with a primary focus on stocks and ETFs. Her commitment lies in empowering individuals to make informed and strategic investment decisions in the dynamic world of finance.

The post 3 Affordable Pharma Stocks to Buy for Portfolio Gains appeared first on StockNews.com

https://www.entrepreneur.com/finance/3-affordable-pharma-stocks-to-buy-for-portfolio-gains/472607