The Trade Desk Shareholders Will Vote Whether CEO Jeff Green Should Keep Supervoting Shares

The Trade Desk shareholders will vote whether to change the voting structure of the company, potentially imperiling CEO Jeff Green’s control, according to an SEC filing.

The Trade Desk is holding a special stockholder vote on September 16 on whether to amend the date in which Green’s super-voting shares expire, or maintain the company’s current dual-class structure. Under that structure, the company offers two kinds of stock: Class A stock, which carries one vote per share; and Class B stock, which comes with super-voting rights that equate to 10 votes per share.

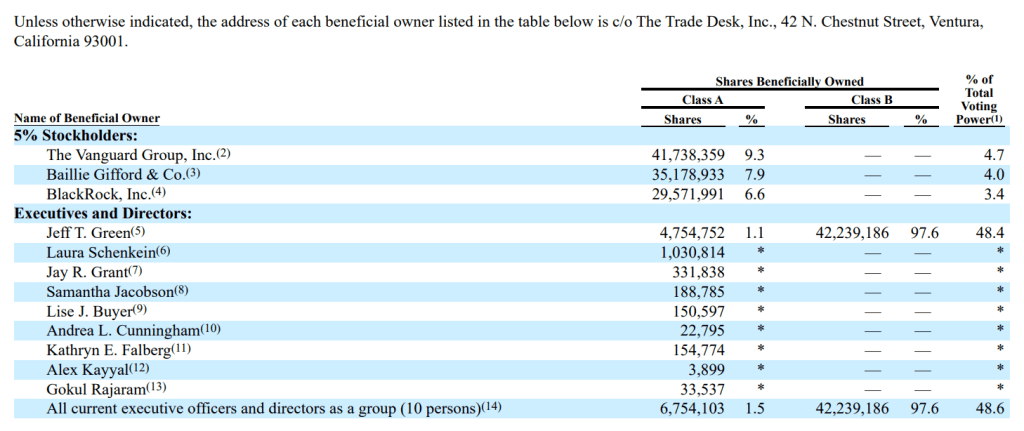

Green, who controls more than 42 million shares of Class B stock and nearly 5 million shares of Class A stock in The Trade Desk, maintains 48.4% of total voting power in the company, according to the filing.

While not required, it’s general practice for companies with dual-class stock structures to have triggers for when those super-voting shares expire, or automatically become Class A voting shares. Those triggers include when Green’s term as chairman and CEO ends, if more than two-thirds of shareholders vote to end it, or at a pre-determined sunset trigger, which is currently set for December 22, 2025. In the filing, The Trade Desk’s board has proposed extending that sunset trigger by 10 years, to December 22, 2035.

In a proxy statement, the company urged shareholders to vote to approve the proposal, citing Green’s tenure as chief executive and The Trade Desk’s high valuation as confidence in extending the sunset trigger. Should shareholders reject it, which analysts say is unlikely in part also because of the dual-class share structure, Green’s position as top decision-maker at the company could be up in the air.

“We have outperformed other ad-tech enterprises during our tenure with a unique approach and dedication to our customers,” the committee wrote, crediting Green’s “foresight, vision and grit.”

The committee praised Green for steering the company through a stock dip in early 2025 and accelerating its rebound, inking new partnerships, and debuting “a flurry of AI-powered innovations.” As such, the group said, “we concluded that it is in the best interest of all of our stockholders to stay the course that has served us so well to date by again asking to keep the Class A and B structure in place.”

The Trade Desk declined to provide further comment.

“My opinion is they’re going to extend it. [Jeff is] not going to give up his super vote,” said Jason S. Helfstein, managing director, head of internet research at Oppenheimer & Co. “While the stock is down from a valuation standpoint, at this point there are plenty of adtech companies that trade at much lower multiples than The Trade Desk does. It’s a very high probability that the board extends super voting shares.”

Dual-class structures have become increasingly common among U.S. tech companies since the early 2000s, spiking in the mid-2010s with major IPOs including Facebook in 2012, Square in 2015, Pinterest in 2019, and Coinbase in 2021, according to data compiled by Jay R. Ritter, a finance professor at the University of Florida.

While the structure can empower visionary leaders, it also limits checks on power. Without such a structure, Green would be forced to bend to the will of outside shareholders on any number of matters.

“If this vote goes against Jeff, he would lose control of the company. He wouldn’t be able to appoint his own board members, and he would essentially have to report to a functioning board of directors of the company,” said a former Trade Desk employee who still has some equity in the company, speaking on condition of anonymity.

The company held a similar vote in 2020 and was set to vote on the dual-class structure every five years thereafter. In that initial vote, the board of directors and investors chose to extend the dual-class arrangement.

In essence, the request asks stockholders to trust Green’s instincts over their own voting power. Whether investors will agree with this recommendation is yet to be seen.

The Trade Desk’s market value soared as high as $69 billion in December of 2024, nearly 70 times its 2016 IPO valuation, before sliding to around $25 billion today. Despite its largely positive revenue, earnings, and margins trendlines, the stock—and Green himself—have attracted recent scrutiny.

Wall Street reacted harshly to Green’s commentary on an August 7 earnings call on which he brushed aside concerns about intensifying competition from Amazon. “I think Amazon is more of a potential partner, honestly, than it is a long-term competitor,” he said. Millions of dollars in marketing spend had funneled out of The Trade Desk and to Amazon’s DSP this year, as ADWEEK previously reported. The company’s shares crashed nearly 40% in the days after the earnings call.

Correction, Aug 29 at 9:45 a.m. ET: This story has been corrected to clarify the details of the proxy vote.

https://www.adweek.com/programmatic/the-trade-desk-shareholders-will-vote-whether-ceo-jeff-green-should-keep-supervoting-shares/