Why Banco de México is printing banknotes at maximum speed

May 25, 2021 7 min read

This story originally appeared on Alto Nivel

Written by Guillermo Barba.

Editor’s note: This text belongs to our Opinion section and reflects only the author’s vision, not necessarily the High Level and Entrepreneur en Español point of view.

As a result of the global economic crisis caused by the mismanagement of the Covid-19 pandemic, central banks and governments from all latitudes have engaged in the largest injection of monetary stimulus in history.

True to the only monetarist and Keynesian recipe they know, they have resorted to the usual “stimuli”: artificially depressing interest rates and injecting huge waves of public spending, especially in developed economies.

In the case of the US Federal Reserve, the injection of liquidity remains at levels of 120 billion dollars a month, with a target range for the federal funds rate between 0.0 and 0.25 percent.

In our country, Banco de México (Banxico) also threw itself into the arms of the stimulation of cheap credit, despite the fact that, unlike the Fed, it does not have a dual mandate to maximize employment and contain inflation. The priority objective of our Central Institute is to maintain low and stable inflation.

Still, Banxico also cut its target interest rate again this year to just 4 percent in February. Although it is very likely that its Governing Board would have wanted to continue with that rate reduction towards the previous minimum of 3 percent, the truth is that the inflationary pressures seen in 2021 not only did not allow it, but now the pressure on rates interest is up.

With such low yields and an annual inflation rate of 6.08 percent in April, it is clear that those sacrificed in Banxico’s monetary policy have been Mexican savers.

Although the expectation that inflationary pressures will be “transitory” is insisted upon, here we have elaborated on the reasons why this will hardly be the case.

In this sense, there is a monetary factor that will undoubtedly do everything but help the central bank to meet its self-imposed goal of achieving annual inflation of 3 percent, plus or minus one percentage point: the monetary aggregate M1.

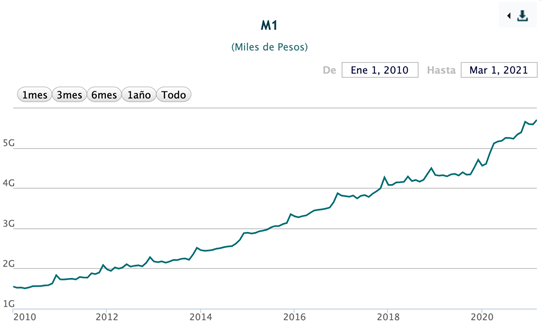

Image: Banxico

This aggregate is made up of banknotes and coins held by the public, plus deposits of immediate demand in banks, Savings and Loan Societies (SAPs), Popular Financial Societies (Sofipos) and Cooperative Savings and Loan Societies (SCAP).

The question from the graph above is: why in 2020, the year of the worst economic collapse in almost a century, did the growth of the M1 aggregate skyrocket?

And it is that in 2020 – when the economy collapsed 8.2 percent-, the monetary base expanded 17.9% in real annual terms, while the monetary aggregate M1 increased by 16.4% in real annual terms.

However, the worst data was obtained last February, when the monetary base grew 20.5% in real annual terms, while M1 increased by 16.9% in real annual terms. That size is the real “inflation” of the currency in Mexico, which has Banxico printing banknotes at maximum speed to satisfy demand.

There are several reasons that explain this apparent paradox between an economy that is contracting very strongly and a monetary base catapulted to the upside.

Banxico officials have tried to give explanations that range from increases in the limits for the use of cash in ATMs by banks; the convenience of families in increasing liquidity as a precaution against spending contingencies or to avoid going to branches to make withdrawals, and they even speak of annual promotions such as “El Buen Fin” to justify it.

However, the real problem is much more fundamental, so much so that it is also occurring in other countries such as Spain or the United Kingdom.

In fact, in the Cash in the time of Covid study published by the Bank of England (BoE) in November 2020, it highlights that “During the Covid-19 (Covid) pandemic, the way in which people use cash has changed, and it is used less for transactions, “but he notes:” People spend less cash, but the total value of banknotes in circulation has increased as people seem to choose to have more cash. “

These findings are consistent with data from Banxico that indicates that due to Covid-19, consumers began to move away from cash in their transactions to adopt digital forms of payment. Almost 5 million Mexicans would have reduced the use of bills and coins in 2020, while 3 million left the cards to use mobile applications.

The BoE researchers state that “The apparent paradox is explained by the increasingly important role of cash as a store of value” (boldface mine). And so it is.

Unfortunately, with the downward manipulation of interest rates, it is worth more for people to save “under the mattress” to have it available at all times, be it in cash or in a checking account, than to sacrifice liquidity to invest it in traditional instruments at term that pay negative returns in real terms, or in afores.

The real paradox then is that with a monetary system that is only sustainable through increasing debt issues, our money IS NOT really a good store of value, although some believe it.

People’s accumulation of cash is like this, a simple intuitive response that something is wrong with the monetary system, with banks and the economy in general, but that it also tells us about the lack of information and financial culture that is needed so people understand that keeping the cash is a losing bet. What they need is to get closer to real investment options in times of depressed rates.

It is therefore not enough to accumulate bills. We must protect the purchasing power of our savings and income, shield them against inflation, against endless monetary expansion and the political-economic unreason of our leaders.

What is happening today with Banxico, as worrisome as it may be, pales in comparison to the brutal monetary corruption that is happening right now around the world, and those who do not have true havens of value in their portfolio – such as physical gold – will pay for it with the impoverishment of their families. Unfortunate but true.

https://www.entrepreneur.com/article/372779