Modern Western society has expectations when it comes to retirement. Ideally, couples of retirement age should have a large enough nest egg to support them in their twilight years, meaning they have a well-balanced portfolio suited to their risk appetite.

In retirement, couples often have a 401(k), an IRA, diversified investments in mutual funds, stocks, and bonds, plus some cash in the bank and Social Security. Furthermore, many retirees prefer annuities to provide them with steady paychecks and protect them—at least in part—from market risk.

However, the changing landscape of retirement may mean that retirees may be deficient in one or more of these investments. Many reasons contribute to financial difficulties in retirement. People are living longer these days. A longer average lifespan leads to a shift in demographics or graying societies.

Life expectancy in the US in 2023 is 79.11 years. In 2000, it was 76.75. In 1980, it was 73.70. In 1960, it was 69.84. The nearly steady growth from the mid-20th century to the present and current projections shows that people are living longer than ever and will only continue to break previous records. Graying societies mean that the number of older people is increasing—a phenomenon attributed to developed countries—with implications for healthcare and economics.

As the number of people aged 65 or older increases, so does the incidence of depleted retirement savings. Moreover, the rising cost of living and inflation during retirement force children to provide financial assistance to their aging parents. The US Bureau of Labor Statistics computes the average American’s annual wages across all occupations as USD 61,900. By age 67, therefore, the average retirement account should contain at least USD 619,000, per guidelines of investment firm Fidelity.

Not everyone can save up and maintain a sufficient retirement account. The average retirement savings in the US is USD 65,000 per household—far from the ideal amount calculated by Fidelity. Moreover, as many as 25 percent of Americans have no retirement savings.

The changing statistics shaped by demographics and the economic climate lead to the current dilemma. Kids today support aging parents more than ever and take on more financial responsibility as they struggle to navigate inflation, economic uncertainty, increasing cost of living, and graying society.

Dilemmas Faced by Aging Parents as They Retire

What is considered an adequate retirement plan? It depends on your needs, resources, preferences, lifestyle, and risk appetite. You need to ask yourself whether you want something resembling a steady paycheck, a flexible portfolio, or something riskier and positioned for growth.

Gone are the days when basic pension plans and Social Security alone could cover the cost of retirement. While Social Security is one of the essential foundations for retirement, it can only replace about 40 percent of the average American’s salary.

About 20 percent, or one in five retired couples, and nearly half (45 percent) of single retirees depend on Social Security for as much as 90 percent of their retirement income—an alarming figure. Another problem in retirement planning is the proper allocation for emergencies and health care needs, which tend to deplete retirement savings when not anticipated.

Adult Children Juggling Financial Responsibilities

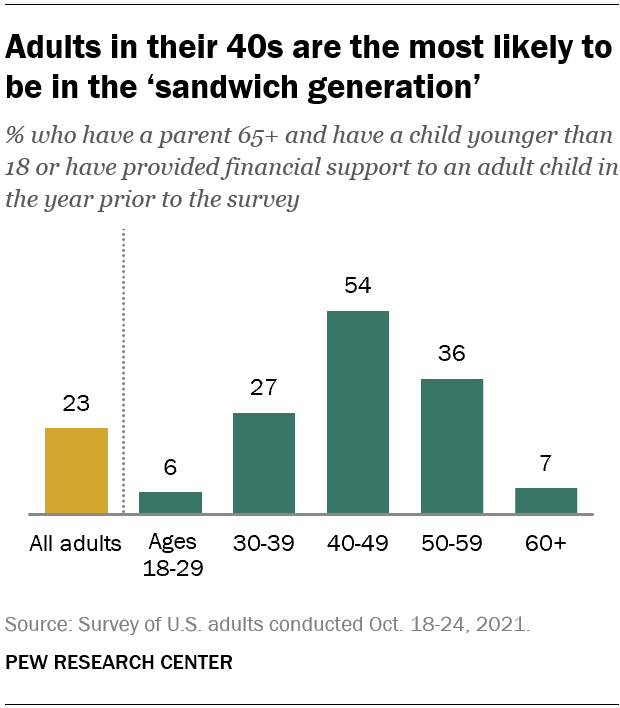

If you read articles on retirement or finance, you may come across the term “sandwich generation.” What is the sandwich generation? These Americans are caught between an aging parent or aging parents and raising their children. It pays to know that the US is already a graying society. The demographic aged 65 and older is estimated to double by 2050.

Who are the caretakers? The sandwich generation typically covers middle-aged individuals, which means the majority are Gen X. However, it may also refer to older millennials or even Gen Z. According to Pew Research, over half—54 percent—of this age group have a parent 65 or older.

Graph from Pew Research Center

{kind=link}

According to the AARP, 32 percent of midlife American adults with at least one living parent provide financial support. Moreover, 42 percent of Americans expect they will eventually have to support their aging parents. This type of financial assistance happens regularly. It covers ongoing expenses like groceries and household items versus one-time situations.

In addition, the AARP surveys found that 54 percent of midlifers gave USD 1000 or more to their parents in the year prior. Among such midlifers, the concerns were showing. Nearly half (47 percent) were worried about their ability to support their aging parents financially. Such results show that a good number of Americans are facing difficulties funding their retirement as resources are being funneled elsewhere.

The Social Changes Leading to Adult Children Supporting Parents in Retirement

Which particular societal shifts lead to a backdrop that drives children to help their aging parents financially and augment their retirement savings? Here is a list:

Changing Economic Realities

One significant factor driving adult children’s financial support is the lack of retirement savings among older adults. Rising interest rates, inflation, and talk of a recession all affect retirement readiness.

Data from the Federal Reserve’s Survey of Consumer Finances shows that households’ median retirement account balance needs to catch up to what is necessary for a comfortable retirement, leading to increased reliance on familial support. Hence, families need to adjust their plans for their financial future and prepare emergency savings for the future.

Rising Cost of Living

The cost of housing, healthcare, and education has been steadily increasing. Older adults may have yet to compute such increases in expenditures and, as a result, have difficulties making ends meet with limited retirement funds.

Moreover, credit card debt among both baby boomers and their adult kids factors into financial issues. Inevitably, adult children are filling in the gaps to secure a better quality of life for their aging parents and improve their financial situation.

Longer Life Expectancy

Today, we are witnessing an extended retirement period, wherein improved healthcare, advancements in medical technology, and a greater emphasis on wellness have led to longer life expectancies. Longer lives represent medical and scientific improvements. However, they also lead to financial issues and decrease financial security.

The time frame for accumulating a decent nest egg may have become longer and, in some cases, unattainable.

Healthcare costs have been rising steadily. A perfect storm happens when you couple longer life expectancy with increasing healthcare costs. Retirees often face higher medical expenses, including long-term care needs, which can quickly deplete their savings. Financial sacrifices may be necessary to sustain long-term costs in healthcare.

Shifts in Social Support Systems

Unlike in the past, public welfare programs are becoming increasingly strained. General welfare systems, such as Social Security, are experiencing increased pressure due to changing demographics—that is, a growing elderly population means more lavish government spending. As a result, there are concerns about their long-term sustainability. There may be reduced benefits and uncertainties surrounding public support.

On top of concerns about Social Security, society is also facing the dilemma of inadequate private pensions. Many employers have shifted towards defined contribution plans such as 401(k)s. These plans place the burden of retirement savings on individuals. This shift has resulted in lower retirement savings and a greater reliance on familial support.

Pros of Kids Financially Supporting Retiring Parents

While people see many disadvantages in allocating for the needs of aging parents while trying to save for their retirement, society sees some benefits. Only some things are quantifiable by money, and many find fulfillment in caring for their aging parents. There is a cultural context to this that people cannot ignore.

Values-wise, Americans overwhelmingly believe that adult children should assist their parents financially when needed. Many believe this is an inherent responsibility. Furthermore, the belief runs among various demographics—across genders, races, and multiple levels of educational attainment. In summary, the following are the pros of kids financially supporting their retiring parents:

Fulfilling Filial Responsibility

In some cultures, filial duty is significant, and a gesture of support for aging parents may be considered a virtuous act with positive interpersonal benefits.

Tax Benefits and Deductions

Are there potential tax deductions for supporting aging parents? Tax deductions should be an interesting incentive for helping them, but there are indeed some tax benefits if you are resourceful enough. Examples of elderly care tax breaks include being entitled to a bigger stimulus check, getting USD 500 tax credit if a parent qualifies as a dependent, and receiving dependent care credit if you hired someone to take care of a parent so you could work, which could mean up to 50 percent off your adult day care up to a USD 16,000 limit.

Furthermore, it would help if you looked into your employer’s dependent care benefits. The typical offer is just for child care, but some might add elder care to the package. If you paid for a parent’s hospital stay, you could have the qualified medical expense if it is over 7.5 percent of your adjusted gross income or AGI.

Maintaining Family Cohesion

In some cases, support for parents could foster better family bonds, improve emotional relationships, and promote better intergenerational communication.

Cons of Children Financially Supporting Aging Parents

Nowadays, there are disadvantages to being fully or partially responsible for your aging parents’ financial needs. The following are the possible pitfalls of having to shoulder the financial responsibility of aging parents:

Aggravating Existing Financial Constraints

There may be an impact on the caregiver’s income, home ownership, and ability to reach financial goals. Moreover, providing financial support for parents may increase struggles with debt, student loans, and other financial obligations.

It could also affect the quality of life of the next generation. The household budget may shrink, and there may be less allocation for the rest of the family, especially for dependent children or minors.

Negative Impact on Family Dynamics

Over time, personal conflicts and strained relationships may develop as a result of unequal burden distribution and feelings of resentment or obligation.

Over-Dependence and Loss of Autonomy

Parents may develop low self-esteem or lose their sense of independence by becoming overly reliant on their children.

Tips for Assisting Aging Parents Financially

Even as you are sincere in your intentions to help your parents, it’s crucial to have a strategy for assisting them. The following are some quick tips as you assist your aging parents financially:

Be Transparent

It’s important to remind your parents that you have your own needs too. Caregivers should pay attention to their financial well-being, so open communication between generations is essential. Furthermore, transparent communication is crucial to sound financial planning, budgeting, and strategizing long-term care and health insurance options. When you want the solutions to be sustainable, communicate openly and regularly.

Downsize

Explore downsizing or placing parents in senior living communities. Downsizing or relocation may ease tension within the household and have the added benefit of being cheaper overall, depending on the circumstances.

Take Advantage of Social Benefits

Explore available social programs and benefits that can help reduce costs.

Encourage Independence, Even in Small Ways

Even if your parents are 100 percent financially dependent on you, you can slowly wean them off total or high levels of dependence by exploring part-time employment suited for retirees to improve their income streams and maintain a sense of purpose.

Even if the whole endeavor is financially and emotionally daunting, striving for balance, setting boundaries, and constantly exploring alternatives are essential.

Supporting Aging Parents? Safeguard Your Financial Stability

The transition of Western society towards adult children supporting their parents in retirement reflects longer life expectancies, changing economic realities, shifting family dynamics, and strained social support systems.

The combined dilemma of rising living costs, inadequate retirement savings, and longer life expectancies has created a need for intergenerational financial cooperation. Still, the decision of adult children to support their parents when they retire is profoundly personal and complex, as it touches on values, ethics, and cultural beliefs.

Providing support for retirement-age parents can strengthen family ties. However, it can also create emotional and financial challenges. Children should be bold and unafraid to ask hard questions. They should discuss financial planning, boundaries, and alternatives with their parents.

While the scenario is never easy to navigate, keeping your head above water and finding a balance between personal financial responsibility and supporting loved ones through life difficulties is essential. You can ensure balance through open communication, careful financial planning, and a clear understanding of economic circumstances.

While the support targets short to medium-term needs, the key to safeguarding financial stability despite the additional burden is to focus on long-term goals and explore alternative means of support. Ultimately, the goal is sustainability and eventual financial comfort for all parties.

The post Should Kids Financially Support Their Parents When They Retire? appeared first on Due.

https://www.entrepreneur.com/finance/should-kids-financially-support-their-parents-when-they/458806