Right now is a tricky time to manage investments. Stocks, real estate, gold, and crypto are all in bear market territory with a huge chance that the recession will worsen this year.

Due – Due

Due – Due If you’re looking to make a risky bet, you could consider shorting the market in various capacities.

However, if you’re looking to allocate capital as safely as possible, here are some options with (relatively) high returns.

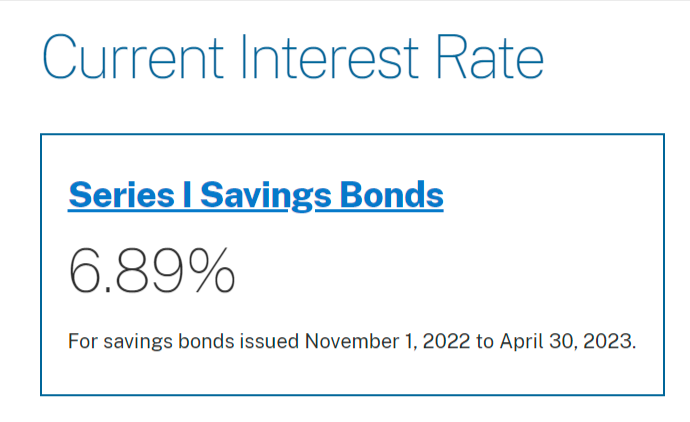

1. I-Bonds

US government-backed bonds are about as safe as it gets. The Series I Savings Bonds accrued at a whopping 9.62% in 2022, and now are offering 6.89%.

Source: TreasuryDirect.com

Interest on the bonds is tax deductible on your federal income taxes. (Though the investment of principle isn’t.)

These interest rates are pegged to inflation, and they change every six months. So if inflation goes up or down, the rates will go up or down, too.

The downsides to this investment involve time and investment caps.

You have to keep the bond for at least one year to gain any interest. If you redeem the bond before holding it for five years, your last three months will not be paid interest as a penalty.

The investment cap is $10,000 per person per year. This is more flexible than it seems.

You’re allowed to invest $10,000 for every person in your household, including minors. So if you have a family of four, you can invest $40,000 per year.

Businesses can also invest up to $10,000. So if you have one or more businesses, that gives you additional investment opportunities as well.

The calendar year limitation is quite flexible too because you don’t have to wait 12 months before making your next investment.

If you already maxed out your I-Bond allocations even as recently as December 2022, you can make your next investment in January 2023.

The traditional inflation hedges, gold and silver, actually declined in price in 2022. So the I-Bond may be your best bet to stay ahead of high inflation.

2. Pay Off Your Mortgage

Source: Photo by Scott Webb from Pexels

This may not be the sexiest investment of the year, but it’s guaranteed to pay off.

If the stock market and other investment markets have a down year, paying off your mortgage may be one of the best returns you can get.

Paying off your mortgage early can save you tens of thousands of dollars in interest. It also decreases your overall financial risk and eliminates what is most likely your biggest monthly bill.

Say you’ve been in your house for three years and have a balance of $300,000 on your home loan at a 3.5% interest rate. The loan term is 30 years.

If you pay an extra $1,000 per month, the loan will be paid off 12 years and 2 months earlier than it would have been.

More importantly, you’ll save $91,824 in interest. (Based on these Calculator.net calculations.)

If you analyze your return on investment, you’ll net 4% per year in annualized returns. (Based on this ROI calculator.)

That may not be record-breaking, but it’s a guaranteed return on an asset that you own 100% of and have insured. Anyone can do it.

Even high net-worth individuals often have huge mortgages, so this advice applies to people across the economic spectrum.

Don’t have a mortgage? The same advice applies to student loans and car loans.

Of course, credit cards are the best debt to pay off because of their high-interest rates. In my opinion, credit card debt should be the first investment priority of anyone who has it.

3. Annuities

Fixed-income annuities are like setting up your own private pension plans. You can invest in them while you’re healthy and working, with the expectation that they provide money for you as long as you live.

The biggest financial risk that any of us face is that we’ll outlive both our working years and retirement savings.

Annuities fix this by guaranteeing income for retirement. This is one reason why many economists recommend annuities.

There are many different types of annuities, and like any investment, they can vary quite a bit. Some contain more risk than others.

Still, if you’re looking for an investment alternative to the huge movements in the stock market, annuities offer an opportunity to diversify your portfolio and shield you from market fluctuations.

As with all investment opportunities, you should make sure that you understand what you’re investing in and speak with your financial advisors before proceeding.

Annuities are particularly tricky in this regard because they are usually offered by life insurance salespeople who get huge commissions for selling them. But if an annuity strategy is smartly employed as part of a balanced portfolio, it can offer a consistent retirement income source that few other products can match.

4. Invest in Art

This is an unusual one that is normally reserved for the wealthy.

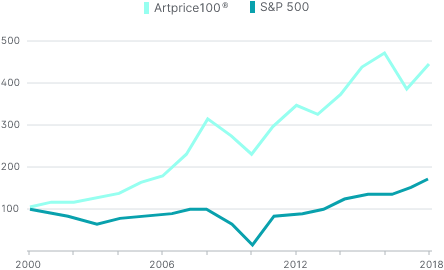

However, as alternative investment platforms like Masterworks and Yieldstreet will tell you, the entire asset class of art has outperformed the S&P 500 by a healthy margin since 2000.

The Artprice100® Index vs. the S&P 500. Source: Yieldstreet

It also has a low correlation to the price movements of stocks and bonds.

Normally the cost and expertise needed to buy a $5,000,000 painting make art inaccessible to the average investor.

However, alternative investment platforms, like those mentioned above, make it affordable for the average investor to buy a share of a valuable piece of art.

One of the main downsides to investing in art is the asset itself. Most asset classes are necessarily boring and unoffensive.

Conversely, many people consider contemporary art to seem silly at best. Or downright repulsive at worst.

Source: Artist JEAN MICHEL BASQUIAT via Masterworks.com

If you can hold your nose regarding the appearance of the asset itself and learn to understand how the art market works, it can be a valuable investment.

Also, keep in mind that this is not a liquid investment. You’ll want to hold onto your ownership shares until the underlying asset gets sold, which could take 1-10 years.

5. Buy Farmland

Like art, this one is off the beaten path for the average investor. And historically, it requires large capital investment and considerable expertise to get involved.

Also like art, farmland is now accessible to a wider group of investors through multiple investment platforms. A few platform examples include Acretrader, Farmfolio, FarmTogether, and many more.

Many of these platforms require that you be an accredited investor to invest, but some don’t.

Acretrader claims that farmland has an average 11% historical yield, without the volatility of stocks and real estate.

Source: Acretrader

I was particularly surprised to learn that farmland prices don’t mirror commercial real estate, but it makes sense. Farmland supply and demand differs greatly from commercial buildings and land, which are mostly urban.

It’s important to note that farmland investments do not involve the farm operations themselves.

Many farmers lease their land, and the buildings, livestock, and farming businesses themselves are not part of the investment.

The main downside to farmland is that it’s not liquid. You won’t get your money back until the land is sold years later.

If your investment horizon is at least 5-10 years, then it could be a good option for diversification and safety.

6. Invest in Your Own Business

Venture-backed companies typically invest all of their profits back into the company for rapid growth. However, most small businesses don’t operate this way.

If you’re a business owner, now might be the perfect time to think more like a startup and plan your expansion. If your business is in good shape financially, spending on growth could be your smartest investment.

Real business expenses like advertising and inventory are tax deductible, so any new business cost that you take on will lighten your tax burden.

As mentioned earlier, many small business owners don’t allocate capital into their business at the same level they would their own 401(k). Why not?

A smart growth strategy can be your best weapon in protecting your business as the recession gets worse in 2023.

Of course, you don’t want to spend frivolously or on expenses that won’t promote growth.

But if your business has a good track record and you believe in your operation, it could be a solid investment path.

7. Your Savings Account

High inflation in 2022 turned off many investors from saving money in a bank account.

On the contrary, I would argue that bolstering your cash reserves may be the smartest move you can make right now.

For starters, interest rates are high. Saving account interest rates are higher than they’ve been in over a decade. Getting 3% interest on savings is entirely doable.

Second, it never hurts to have a lot of cash on hand during a recession. As they say, “cash is king.”

If you lose your job or any of your income sources get jeopardized over the next year, a healthy cash reserve will be your best friend.

Third, and most importantly, there is a very high probability that deflation will set in. There are loads of indicators that the economy will get worse and that markets will continue to tumble.

Why not build your cash reserves to buy back in at the bottom?

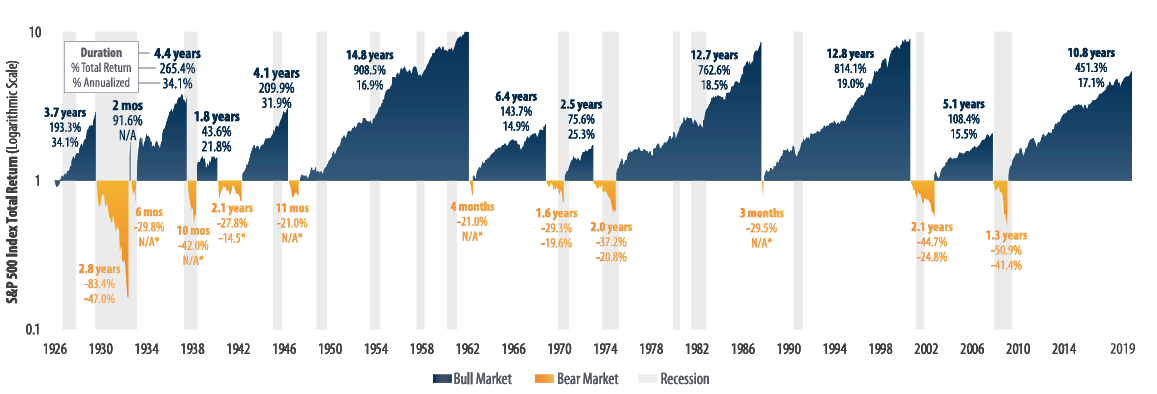

Over the past 100 years, the average stock bear market lasts 1.3 years and has a typical loss of 38%.

Source: First Trust via UIdaho.edu

In more recent years, bear markets have been even longer and lower:

- The 2007-2009 bear market was 1.3 years and went down 50%

- The 2000-2002 bear market lasted 2.1 years and went down 45%

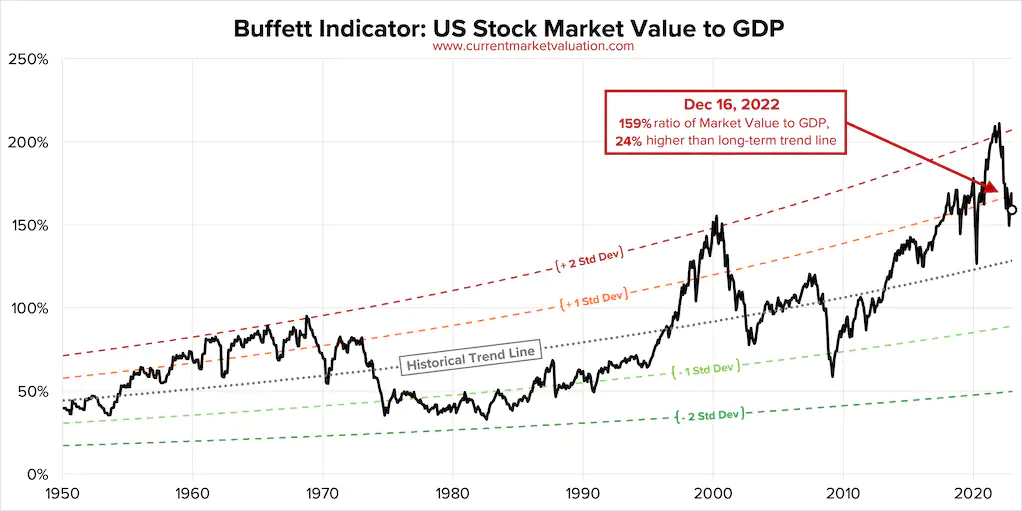

Warren Buffet famously cites the GDP to stock market valuation ratio to measure the state of the overall market. Some people call this the “Buffett Indicator.”

At the time this article was written, markets are “Significantly Overvalued.”

Source: CurrentMarketValuation.com

In 2022, the Federal Reserve demonstrated a high commitment to quashing inflation. They did this by raising interest rates.

If inflation remains the #1 enemy to US economic policymakers in 2023, then the markets will continue to tumble.

What better way to wait out the crash than with a healthy savings account?

Final Thoughts

None of us have a crystal ball. But the markets and the government policies that affect them typically follow patterns.

One of the most difficult parts of investing is controlling your emotions.

Keep your head. Follow a sound strategy. That’s how you’ll make 2023 a great year for your portfolio.

The post 7 Safe Investments with Relatively High Returns for 2023 appeared first on Due.

https://www.entrepreneur.com/finance/7-safe-investments-with-relatively-high-returns-for-2023/443995