This year was largely defined by platforms introducing, fast-tracking or postponing new policies, features, campaign types and offerings in reaction to how consumers and, by extension, advertisers, were impacted by the coronavirus pandemic.

In early March, the approaching crisis began disrupting search and digital ad budgets, with some businesses cutting their ad spend due to supply chain concerns and advertisers in heavily impacted industries, such as travel, halting ads altogether. Despite the initial shock, the industry rebounded in Q3 as COVID-driven commerce contributed to record ad revenue for Facebook, Google, and Amazon.

The pandemic ushered in a new era of e-commerce

Some industries were able to resume normal operations quicker than others, with e-commerce ad spend doubling as social distancing took hold. In light of consumers shifting to e-commerce, Google, Facebook, and other major platforms altered course and expedited existing plans to meet businesses’ new needs.

After eight years of existing as a paid platform, Google Shopping opened up to free product listings in April. Free product listings were also extended to the main search results page via knowledge panels, the company announced in June. Google further shook things up when it got rid of commissions to Buy on Google and integrated with third-parties, starting with Shopify and PayPal. These changes make Google more accessible to a wider range of sellers and may help differentiate it from other marketplaces such as Amazon, which typically charge fees ranging from 8–15% per item sold.

RELATED: FAQ: All about Google Shopping’s free and paid product listings

Bing opened up its Shopping results to free product listings this year as well. It also bolstered its shopping capabilities when it brought visual search to product listings, which may add to product discoverability and help consumers do their comparison shop.

With so many brick-and-mortar stores closing, Facebook launched Shops in May, enabling businesses to establish an integrated online storefront for customers across both Facebook and Instagram. This move signified a major leap towards a unified e-commerce platform and spoke to the increasingly important role of commerce for Facebook, accounting for the company’s largest advertising vertical in Q3.

Pinterest also rolled out several commerce features to its mobile app, including a new “Shop” tab, visual search functionality integrated directly into shoppable Pins and home decor style guides. In May, Shopify merchants gained the ability to turn their catalogs into shoppable Pins (via the Pinterest app in the Shopify app store), providing Shopify store owners with a way to access Pinterest’s over 360 million monthly active users, which may also increase the number of retailers spending ad money on the platform.

Shopify made moves offline as well when it introduced an updated point-of-sale system that integrates online and offline sales capabilities, allowing merchants to serve online, in-store or curbside customers.

Google promoted local pickup options and service provider badges

On the local side, “curbside pickup” badges began appearing in Local Inventory Ads in May, which Google later built upon by boosting the visibility of “nearby” product inventory through new Shopping features. Google local ads also gained Smart Bidding for store sales this year.

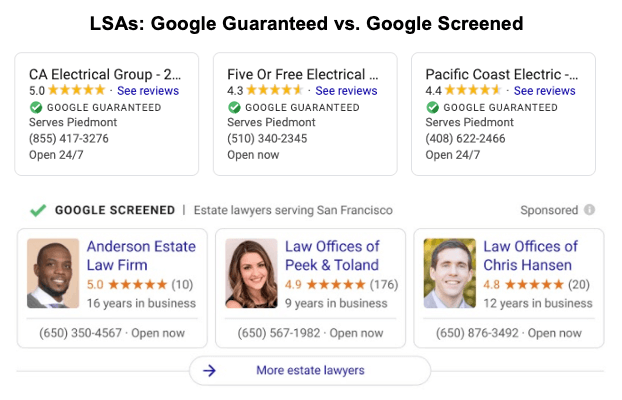

Local Service Ads (LSAs), which Google started as a way for home service providers to promote themselves, were formally launched in July after a successful trial run, along with the Google Screened certification, which is only available to advertisers. Local service providers must meet a minimum review score threshold and be Google Guaranteed or Google Screened to run LSAs.

This type of local ad is displayed at the top of the search results page, and is charged on a per lead basis (instead of per click). Two months after the launch, in September, LSAs became available across European countries and auction-based pricing for LSAs rolled out as a beta test in select markets.

The Google Guaranteed badge became available to non-advertisers through an experimental “upgraded” Google My Business (GMB) profile for $50 per month. The Google Guaranteed and Google Screened badges are “quickly becoming the symbol of trust for Google users,” said contributor Justin Sanger, in his article A new era has arrived in local search: Google’s Local Trust Pack.

Google also ran a number of experiments in Maps: local ads were spotted in the auto-suggest search results and the Google Guaranteed badge started to appear in Maps listings.

Artificial intelligence became more ingrained in how we advertise

Automation continued to be a theme this year, with new audience targeting options and campaign types leveraging machine learning to take the emphasis away from manually managing ads. Google’s policy changes also reflected this trend.

Audiences. Continuous audience sharing was introduced in February, streamlining the sharing process for brands and enterprises that have multiple accounts under a manager account. Custom affinity and custom intent audiences were rolled into custom audiences, which are aimed at providing more targeting flexibility and specificity. Google also employed machine learning to enable advertisers to target predictive audiences based on purchase and churn probability.

Discovery feed. Google finally monetized Discovery feeds this summer when Discovery ads emerged from testing. The company said it can reach a combined audience (across YouTube, Discover and Gmail) of 2.9 billion users — putting it on par with Facebook’s reported 2.99 billion monthly active users. The campaign type also received lead forms as well as the ability to show 4:5 aspect ratio social image assets.

Search terms visibility. In September, Google pushed advertisers another step towards a potential zero-keyword future for search campaigns when it limited Search Terms reporting, citing privacy around user data. The change meant that Google will only include terms that were “searched by a significant number of users,” but did not define what qualifies as “significant.”

This may have made millions in ad spent invisible to advertisers. Digital agency Seer analyzed the initial impact, estimating that for every $100,000 spent on Google search, advertisers received search term data for $71,000 of it. Two months after the change, Tinuiti published a report detailing significant drops in Google-reported search terms; for example, the share of desktop text ads attributed to search queries fell 24 points (from 98% to 74%) between August and September.

Automation. All across the globe, advertisers on Microsoft’s platform received access to responsive search ads (RSAs) — although the format has been available for over two years, and adoption has increased, the debate between RSAs and expanded text ads (ETAs) continues to rage on. As a matter of fact, some marketers were worried that Google was phasing out ETAs, which the company clarified was a test.

RELATED: RSAs: Are they living up to the promise? It depends

Nevertheless, Google’s usage of artificial intelligence indicates that we’re headed into an era of predictive marketing. During Advertising Week, the company continued to progress in that direction when it introduced automated Insights and Performance Max campaigns, and released Video Action campaigns out of beta. In a less-than-subtle move, Google began showing recommendations for switching to broad match; and, with the newly limited search term data it’s showing advertisers, it may be harder to verify that the queries that are triggering your broad match keywords are, in fact, relevant.

The changes that impacted agencies

Google Ads’ poor reputation for providing support plunged further when the company announced in March that small and mid-sized agency partners would be losing dedicated ad rep support. With an overhaul of Google Partners program eligibility requirements announced the month prior (more on that below), some agencies may have felt like Google was leaving them out to dry right as the pandemic began affecting businesses.

To stimulate more advertising, and perhaps earn some goodwill among advertisers, Google pledged $340 million in Ads credits for SMBs, which first began disbursing to qualified advertisers in New Zealand in May.

And, beginning on November 1, Google began passing down its digital services taxes to advertisers in the UK, Turkey, and Austria.

For 2021. In February, Google announced new requirements to maintain Google Partner status, stipulating that at least 50% of eligible users (up from just one certified user with standard or admin access) listed in manager accounts will need to earn Google Ads certification and doubling (to $20,000) its 90-day spend requirement. The company also said that it will be evaluating the optimization score in your manager account to determine whether your agency is meeting performance requirements; this comes as less of a surprise as Google has been increasing its emphasis on the metric. These changes were initially set to take effect in June, but Google decided to postpone them until sometime in 2021 due to the impact the pandemic has had on agencies.

Video advertisers using third-party click-tracking solutions should be aware that Google’s deadline to adopt parallel tracking for Video campaigns has been extended to March 31, 2021.

About The Author

http://feeds.searchengineland.com/~r/searchengineland/~3/WuJLNYFSqIY/ppc-2020-in-review-covid-leaves-its-mark-on-e-commerce-and-paid-search-344987