News that LinkedIn is creating an online freelancing marketplace sent Fivver shares down this week.

4 min read

This story originally appeared on MarketBeat

Fiverr (NYSE: FVRR) shares are down more than 12% this week after multiple sources reported that Microsoft (NASDAQ: MSFT) is building an online freelancing marketplace through its LinkedIn subsidiary.

LinkedIn will grab a nice piece of the online freelancing marketplace pie. That’s not up for debate. The business social network has more than 700 million users, many of whom already use the platform to make freelance connections.

Does the LinkedIn news mean that Fiverr is no longer a viable investment?

Fiverr remains a viable investment because a) there are enough freelancing transactions to go around and b) competition was always priced into the shares.

The projected gross volume of the gig economy was just under $300 billion in 2020; that number is projected to rise to more than $450 billion by 2023. Fiverr’s revenue was $189.5 million for full-year 2020. The company’s take rate – or its revenue as a percentage of its gross volume – is 27.1%.

This means that Fiverr handled just under $700 million of freelancing transactions in 2020, or less than $1 out of every $400 of freelancing transactions.

A lot of growth is priced into Fiverr shares, but the company’s market cap is under $10 billion. If Fiverr processes just 5% of all gig economy gross volume in 2023, it would generate a little over $6 billion in revenue at its current take rate. At less than 2x sales, shares would be an absolute bargain.

It’s unlikely that Fiverr will grow to that level by 2023, but the point is, nobody ever assumed that Fiverr was going to handle 20%+ of gig economy gross volume. Existing competition and possible future competition were priced into shares long ago.

An impressive 2020

Fiverr reported its Q4 2020 numbers last week. Here were some of the highlights:

- Revenue increased 89% yoy to $55.9 million and active buyers grew 45% yoy to 3.4 million. Both revenue and active buyer growth accelerated over Q3 2020 levels.

- Revenue of $189.5 million for full-year 2020 was up 77% yoy.

- The take rate of 27.1% for full-year 2020 was up from 26.7% for full-year 2019.

- Fiverr is projecting that it will generate $277-284 million in revenue for full-year 2021, up 46-50% yoy.

- The company expects an adjusted EBITDA of $16-21 million for full-year 2021, up from $9.1 million in 2020.

The 46-50% revenue growth would be a big slowdown from the 77% revenue growth in 2020. But here’s the deal:

- That growth still tops the vast majority of publicly-traded companies.

- Fiverr will face tough comps from 2020. The fact that the company could grow 50% from 2020 levels is impressive.

Tough road ahead

It’s easy to salivate over Fiverr’s upside. Although the company is probably not going to handle 5% of gig economy gross volume by 2023, what if it gets to that number 2-3 years later? What if Fiverr eventually gets up to 10% of the gross volume?

Shares would obviously go up a lot from here if either of those scenarios come to fruition. But at the moment, Fiverr is trading at more than 30x forward sales. If we have another correction – yes, those sometimes happen – this is the type of stock that will get sold off.

Moreover, Fiverr shares more than 8x’ed in 2020. There are a lot of people sitting on massive profits, which could lead to some profit-taking dips.

How should you play Fiverr?

There is an argument to pick up some Fiverr shares now; you’re getting a discount of more than 12% from where they were four days ago, after all.

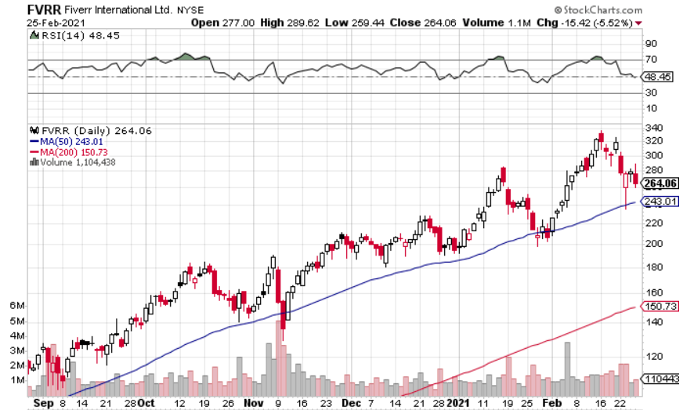

It could pay to wait for a bit though. On Tuesday, shares put in a reversal at the 50-day moving average. But yesterday, shares went up early before closing down more than 5%. Volume was higher than the previous day.

The price action indicates that Fiverr could trade down near Tuesday’s lows. If shares get down to around $245-250, you might want to get in.

At the same time, you might want to start with a small position. A future correction could offer an opportunity to buy shares at a lower price.

https://www.entrepreneur.com/article/366193